Identifying Gender Bias in Banks Is an Important First Step, If a Complex One

Worldwide, income generated from women owned or operated businesses are a critical source of income for families and a key contribution to local and national economic growth. These businesses, however, often don't realize their full potential because they are unserved and underserved. In general women are less likely to receive business credit compared to men, with this disparity attributed to myriad factors, including the smaller size of women-led businesses and their concentration in lower-growth sectors — both largely an outcome of unequal access to resources (World Bank, SME Finance Forum and IFC, 2017; Oxfam, Babson and Value for Women, 2018).

Another factor, however, often unacknowledged, is bias — unconsciously or consciously held by bank staff and embedded in bank processes and decision-making.

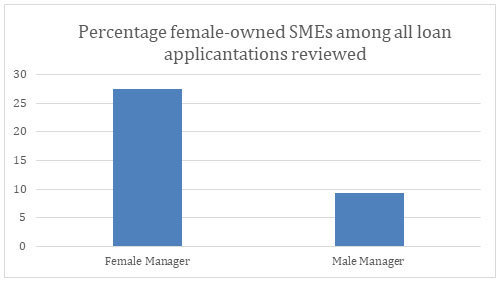

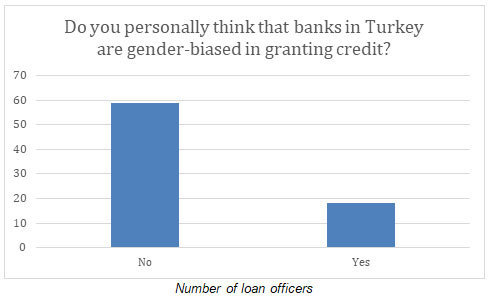

In a World Bank dataset of 77 banks in Turkey, (used in Alibhai et al. 2019) 78 percent of loan officers said they believe that banks do not demonstrate gender bias when granting loans to entrepreneurs. Despite this oft-held belief, it appears that bias may play a role — though it is of course hard to say with certainty. When the same survey asked these loan officers why so few approved loans go to women, 64% of loan officers cited reasons linked to gender stereotypes. For example, loan officers attributed women’s lower credit approval to their own fears of managing credit and to the idea that “women have [a] less active role in commercial life” .

While it is difficult to recognize and root out the specific role that bias plays in defining who gets access to credit, there is a body of work demonstrating that preconceived notions, stereotypes and beliefs about gender can affect decision-making, including decisions made by financial institutions (Beck et al. 2018, Calcagnini, G., et al. 2015, Value for Women, Babson, Oxfam 2018).

Bias in the credit application process can convert into a self-fulfilling prophecy. In various contexts, women have reported feeling anxiety about applying for loans, and assuming that they will not be approved. These perceptions often stem from lived experiences of unequal access or outright discrimination either by banks or in other realms of their lives (Value for Women, Babson, Oxfam 2018).

Biases can also be self-perpetuating. When bank staff see fewer loans going to women, this can reinforce unconscious beliefs that women are less capable entrepreneurs — and in turn, lead to banks continuing to approve fewer loans for women.

Identifying bias is complex, but a key first step is to rooting it out

Bias in credit decision-making is difficult to isolate because of the many variables that may affect credit decisions, including business size, age, revenues, assets and sector. Despite this, it is possible to take steps towards identifying potential bias, including banks analyzing gender gaps in their loan portfolios on a routine basis. Moreover, banks can organize unconscious bias tests with their leaders and staff, or diagnose and address potential sources of bias throughout the credit application and credit approval processes.

The good news is that, because biases are social constructs, they are fluid and can change. There are many ways to challenge our own internal ideas, beliefs and assumptions about our colleagues and customers. Banks can further promote formal structures and training for loan decision making, as a way to reduce officers leaning on bias. They can ensure that internal policies and practices are gender- friendly and inclusive, and create organizational cultures promoting transparency, accountability and equity. In addition to testing for unconscious bias in processes and systems, banks can reexamine their market analyses and value propositions with a gender lens, and create incentives and targets to reach more women. These actions have the potential to improve the ways that institutions function, ultimately unlocking new important opportunities for banks to serve more women and reach their full market potential.

Other Sources:

- International Finance Corporation. 2017. MSME Finance Gap – Assessment of the Shortfalls and Opportunities in Financing Micro, Small and Medium Enterprises in Emerging Markets. Washington, DC.

- SME Finance Forum (webpage).

- Alibhai, Salman; Donald, Aletheia Amalia; Goldstein, Markus P.; Oguz, Alper Ahmet; Pankov, Alexander; Strobbe, Francesco. 2019. Gender Bias in SME Lending : Experimental Evidence from Turkey (English). Policy Research working paper; no. WPS 9100. Washington, D.C. : World Bank Group.

As CEO and Co-founder of Value for Women, Rebecca has spearheaded the growth of the organization into a globally recognized leader in gender-inclusive business practice. With over 20 years of global expertise, Rebecca leads Value for Women in its efforts to design innovative gender-inclusion products and methods, working hand-in-hand with investors, businesses, banks, financial institutions, development organizations, and corporate foundations.

Salman Alibhai is a Senior Operations Officer in the Finance, Competitiveness and Innovations Global Practice in the East Asia and Pacific Region

Aletheia Donald is a development economist with over a decade of experience investigating what works to promote gender equality. She currently works as an Economist at the World Bank’s Gender Innovation Lab within the Office of the Chief Economist for Africa and leads the Measures for Advancing Gender Equality initiative. Her research experience includes the study of poverty, social norms, labor, and methodological work on survey data collection. Before joining the World Bank, Aletheia was a Research Fellow at Harvard’s Evidence for Policy Design and Head of Research for the NGO Empower Dalit Women of Nepal. She holds a Master’s degree in Economics from Yale University and a PhD in Economics from Sapienza University.